library(tidyverse)

library(ggplot2)

library(plotly) # for 3d scatter plot

# read in csv

treasury_data <- read.csv("seminar-material/treasury.csv", stringsAsFactors = FALSE)Seminar 4

Overview

The goal of seminar 4 is to review the material on Principle Component Analysis (PCA). We will first work through Question 1 in Problem Set 3, before reviewing the coding examples below.

Load packages and data

Data cleaning

# Reshape the data into wide format and remove rows with NA

treasury_wide <- treasury_data %>%

select(data_date, series_name, data_value) %>%

pivot_wider(names_from = series_name, values_from = data_value) %>%

drop_na() # Remove rows with NA

# View the reshaped data without NAs

head(treasury_wide)# A tibble: 6 × 7

data_date `3M` `6M` `1Y` `3Y` `5Y` `10`

<chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1981-09-01 17.0 17.2 17.1 16.6 16.1 15.4

2 1981-09-02 16.6 17.3 17.2 16.4 16.1 15.4

3 1981-09-03 17.0 17.4 17.3 16.5 16.1 15.5

4 1981-09-04 16.6 17.4 17.2 16.5 16.2 15.5

5 1981-09-08 16.5 17.4 17.3 16.6 16.2 15.6

6 1981-09-09 16.4 17.1 17.0 16.6 16.2 15.5# Remove the date column and standardize the data

data_for_pca <- treasury_wide %>%

select(-data_date) %>%

scale() # Standardize the dataPlot data

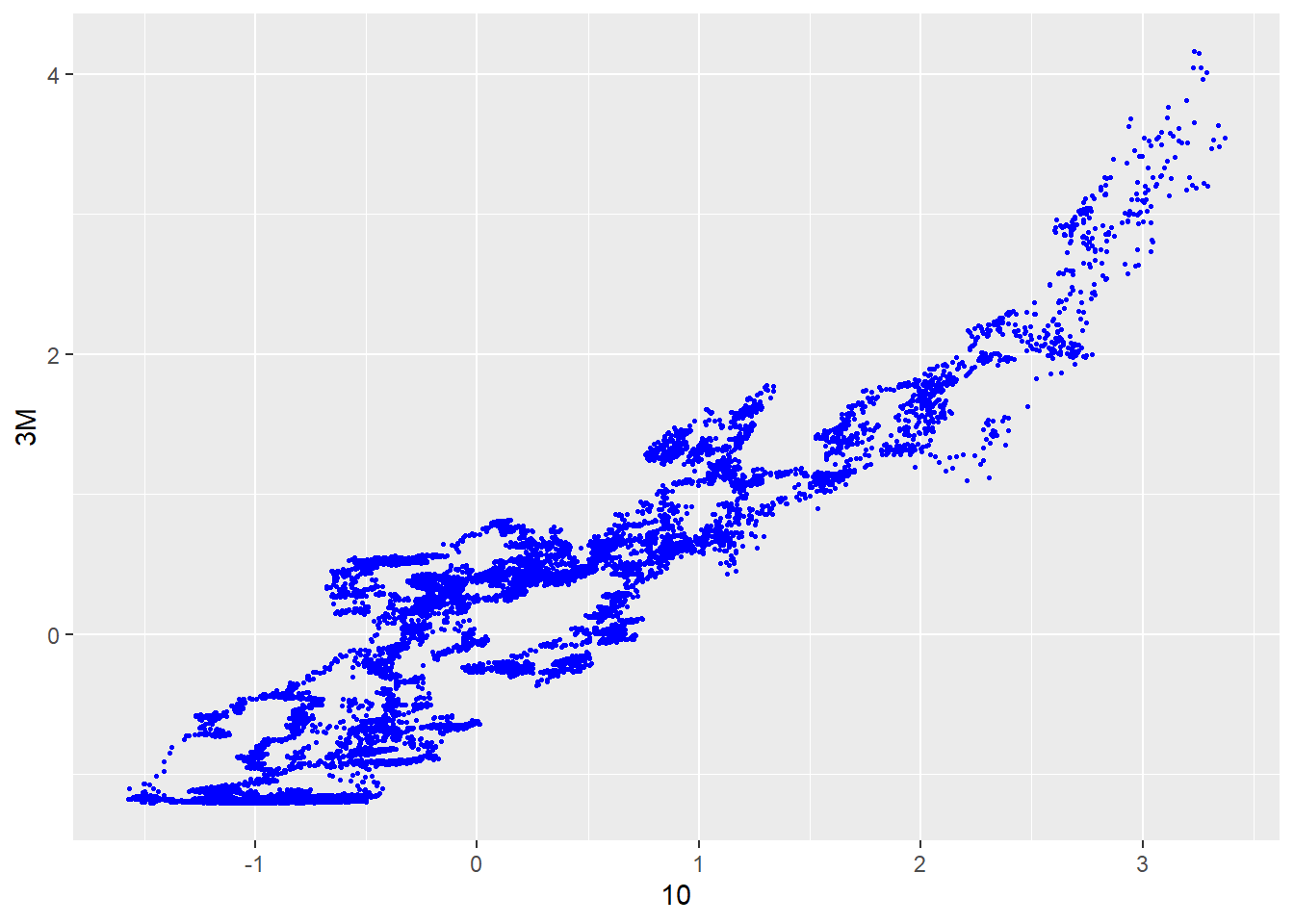

Simple 2D scatter

ggplot(data_for_pca, aes(x =`10`, y = `3M`)) +

geom_point(color="blue", size=0.5)

More advanced 3D scatter

data_for_pca <- data.frame(data_for_pca)

plot_ly(

data = treasury_wide,

x = ~`10`, # Use backticks for column names with special characters

y = ~`1Y`, # Ensure column names exist in your data

z = ~`3M`, # Use backticks if needed

type = "scatter3d",

mode = "markers",

marker = list(size = 5, color = ~`10`, colorscale = "Viridis") # Color mapped to a variable

) %>%

layout(

title = "3D Scatter Plot",

scene = list(

xaxis = list(title = "10Y Treasury"),

yaxis = list(title = "1Y Treasury"),

zaxis = list(title = "3M Treasury")

)

)Perform PCA

# Perform PCA

pca_result <- prcomp(data_for_pca, center = TRUE, scale. = TRUE)

# Summary of PCA

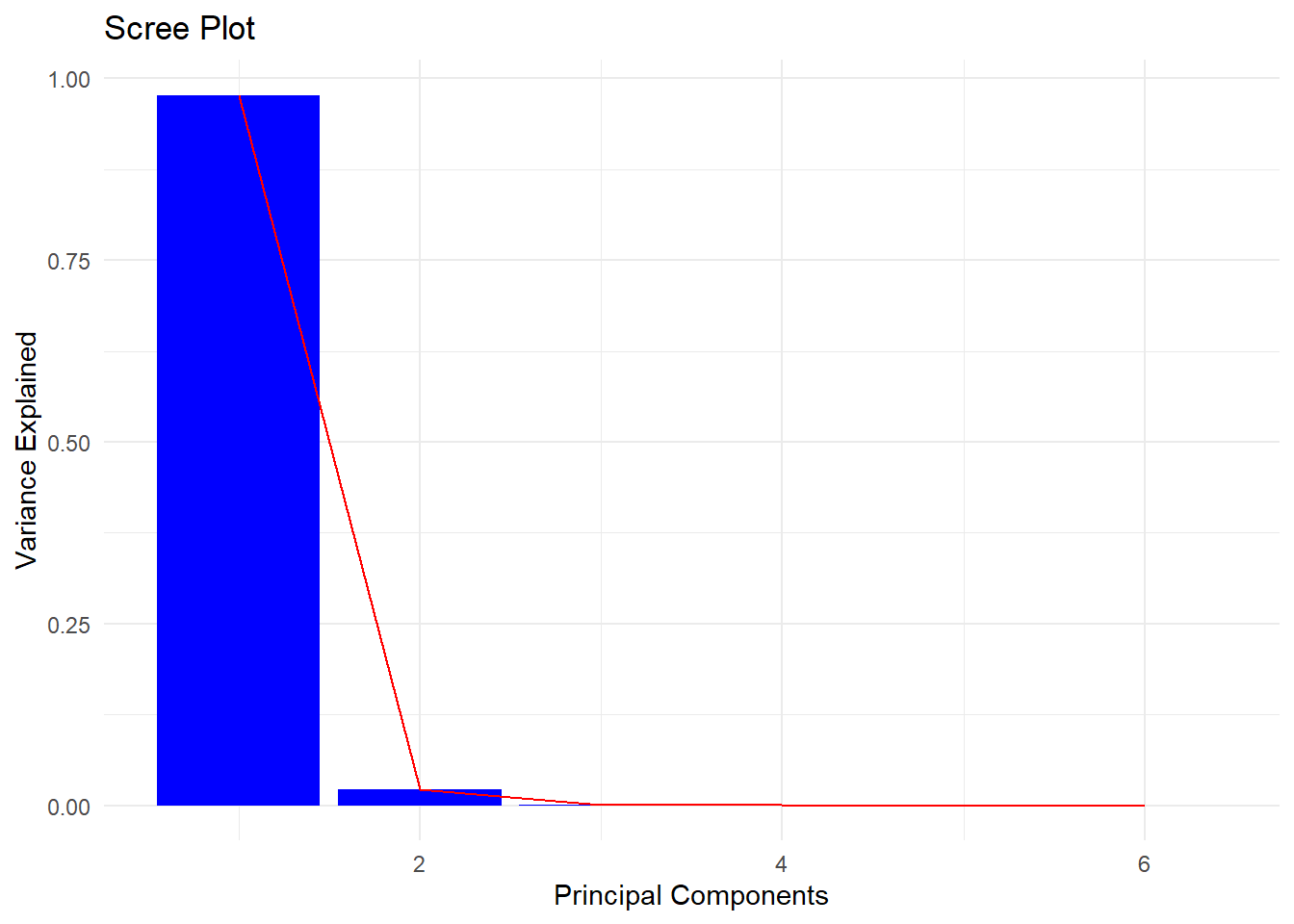

summary(pca_result)Importance of components:

PC1 PC2 PC3 PC4 PC5 PC6

Standard deviation 2.4213 0.35928 0.08123 0.03816 0.01558 0.01117

Proportion of Variance 0.9771 0.02151 0.00110 0.00024 0.00004 0.00002

Cumulative Proportion 0.9771 0.99860 0.99970 0.99994 0.99998 1.00000Plot the elbow-curve

# Scree Plot: Variance explained by each principal component

explained_variance <- pca_result$sdev^2 / sum(pca_result$sdev^2)

scree_data <- data.frame(

PC = seq_along(explained_variance),

Variance = explained_variance

)

ggplot(scree_data, aes(x = PC, y = Variance)) +

geom_bar(stat = "identity", fill = "blue") +

geom_line(group = 1, color = "red") +

labs(title = "Scree Plot", x = "Principal Components", y = "Variance Explained") +

theme_minimal()

Visualize the factor loadings

# Multiply the first principal component scores by -1

pca_result$x[, 1] <- -pca_result$x[, 1]

pca_result$rotation[, 1] <- -pca_result$rotation[, 1]

# View factor loadings

factor_loadings <- pca_result$rotation

print(factor_loadings) PC1 PC2 PC3 PC4 PC5 PC6

X3M 0.4066091 -0.4697895 -0.53519819 -0.4897180 0.2762128 -0.1068292

X6M 0.4087817 -0.3942278 -0.05659105 0.3320350 -0.6434283 0.3873398

X1Y 0.4108823 -0.2637237 0.35580956 0.5196171 0.3736753 -0.4747526

X3Y 0.4120884 0.1333893 0.54113891 -0.3299053 0.3023958 0.5650473

X5Y 0.4092176 0.3707498 0.18399549 -0.3819980 -0.4940162 -0.5208232

X10 0.4018288 0.6317309 -0.50702490 0.3537897 0.1859519 0.1504330Extract principle components

# Define the number of components to retain

n_components <- 6

# Extract the principal components

principal_components <- as.data.frame(pca_result$x[, 1:n_components])

principal_components$data_date <- treasury_wide$data_dateReshape the data to plot.

# Reorder columns so the date is the first column

principal_components <- principal_components %>%

relocate(data_date)

# Convert principal components to a long format for ggplot

principal_components_long <- principal_components %>%

select(data_date, PC1, PC2, PC3) %>% # Keep only PC1, PC2, and PC3

pivot_longer(

cols = starts_with("PC"), # Select all columns starting with "PC"

names_to = "Principal_Component",

values_to = "Value"

)

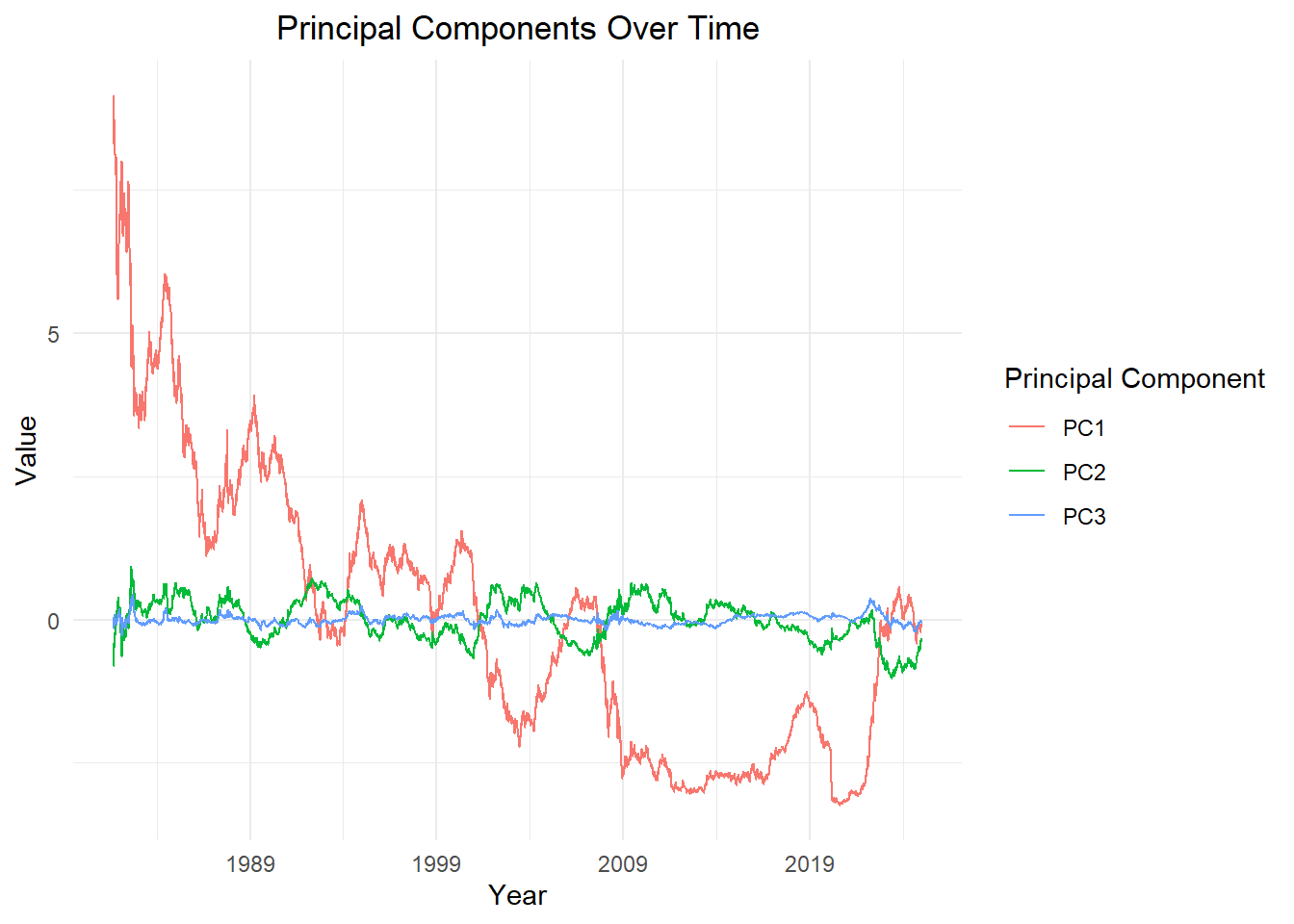

# Plot the data

ggplot(principal_components_long, aes(x = as.Date(data_date), y = Value, group=Principal_Component, color = Principal_Component)) +

geom_line(linewidth = 0.4) + # Adjust line thickness

labs(

title = "Principal Components Over Time",

x = "Year",

y = "Value",

color = "Principal Component"

) +

theme_minimal() +

theme(

plot.title = element_text(hjust = 0.5),

legend.position = "right"

) +

scale_x_date(date_breaks = "10 year", date_labels = "%Y")